Waiting for 3% Mortgage Rates? Why That Strategy Could Cost You More

By Jay Cottrell, Broker Associate with LPT Realty.

NOTE: The views expressed in this article are those of Jay Cottrell and do not represent the views of LPT Realty or any of its affiliates, affiliated companies, or other real estate agents.

Over the past few years, a common conversation has emerged among potential homebuyers:

“I’m just going to wait until mortgage rates go back down to 3%.”

It’s understandable why so many people feel this way. Between 2020 and early 2022, historically low mortgage rates made borrowing extremely affordable. Buyers could purchase more home for the same monthly payment, and the market exploded with activity.

But there’s one important reality many buyers are overlooking:

3% mortgage rates were never normal.

They were the result of extraordinary economic conditions that are unlikely to repeat anytime soon.

Waiting for those rates to return may seem like a safe strategy, but in many cases, it can actually cost buyers significantly more money in the long run

Let’s break down why.

The Truth About 3% Mortgage Rates

Mortgage rates around 3% occurred during a very unusual period in economic history.

In response to the COVID-19 pandemic, the Federal Reserve dramatically lowered interest rates and purchased large amounts of mortgage-backed securities to stimulate the economy. These policies pushed mortgage rates to levels that had rarely been seen before.

For context, here’s a quick look at historical mortgage rates:

- 1980s: Often 10-18%

- 1990s: Typically 7-9%

- Early 2000s: Around 6-8%

- 2010-2019: Roughly 4-6%

- Pandemic period: 2.5-3.5%

When viewed in historical context, today’s rates are much closer to normal market conditions than the ultra-low rates seen during the pandemic.

The expectation that rates will simply return to 3% ignores the economic factors that caused them to drop that low in the first place.

Why Lower Mortgage Rates Increase Buyer Demand

One of the most important dynamics in real estate is the relationship between interest rates and buyer demand.

When mortgage rates fall, monthly payments decrease. That means buyers can afford more house for the same payment.

As affordability improves, more buyers enter the market.

The result is simple:

Lower mortgage rates lead to higher demand for homes.

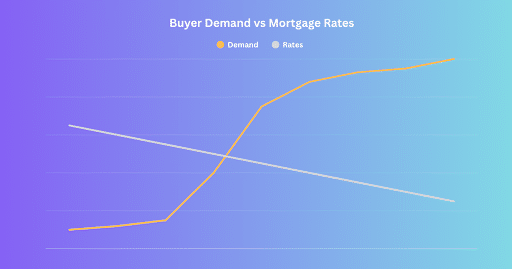

Here’s a conceptual look at that relationship.

As mortgage rates drop, buyer demand tends to increase significantly.

When borrowing becomes cheaper, buyers who were previously on the sidelines often jump back into the market. This increases competition for available homes.

And that’s where the real issue begins.

More Demand Usually Means Higher Prices

Real estate prices are driven primarily by supply and demand.

When buyer demand increases faster than housing supply, prices tend to rise.

We saw this play out dramatically during the pandemic housing boom.

Record-low mortgage rates led to:

- Massive buyer demand

- Multiple offer situations

- Homes selling above asking price

- Rapid home price appreciation

In many markets, home prices increased 30-40% in just a few years.

This is the key issue for buyers who are waiting for lower rates. If mortgage rates fall significantly again, buyer competition will almost certainly increase.

That competition can push prices up quickly.

The Hidden Risk of Waiting

Many buyers assume that waiting for lower mortgage rates will make buying more affordable.

But the math doesn’t always work out that way.

Let’s look at a simplified example. We’ll assuming a 30-yr mortgage with buyer putting 10% down and won’t account for taxes or insurance.

Scenario 1: Buy Today

- Home price: $350,000

- Down payment: $35,000

- Mortgage rate: 6.5%

- Potential Payment: $1,991.01

- Total Cost of Mortgage: $716,765

Mortgage rate drops to 5.5% and increased buyer demand pushes price to $400,000.

- Home Price: $400,000

- Down payment: $40,000

- Mortgage Rate: 5.5%

- Potential Payment: $2,044.04

- Total Cost of Mortgage: $735,855

Even though the interest rate is lower, the buyer in the second scenario may end up paying more overall because the purchase price increased.

Remember:

Interest rates can change.

The price you pay for a home cannot.

The Strategy Many Smart Buyers Use

Because of this dynamic, many experienced buyers follow a simple strategy:

“Marry the house, date the rate.”

Yes, this statement is cliché and overused by real estate agents and mortgage professionals, however…..

This means:

- Buy the right home when you find it.

- Lock in the purchase price.

- Refinance the mortgage later if rates fall.

Refinancing allows homeowners to replace their current mortgage with a new one at a lower interest rate and probable lower payment when market conditions improve.

Historically, many homeowners refinance multiple times over the life of a loan. What they cannot change is the original price they paid for the property.

Why Prices Rarely Fall When Rates Drop

Another misconception is that home prices will fall when mortgage rates decline.

In reality, the opposite usually happens.

Lower interest rates increase affordability and expand the pool of potential buyers. This increase in demand often places upward pressure on prices.

Prices tend to decline only when one of two things occurs:

- A major economic downturn

- A dramatic oversupply of housing

Experts are not predicting much of a mortgage rate drop for 2025.

Currently, most housing markets across the United States still face a housing shortage, which helps support property values.

Supply Is Still Limited

As mentioned, another factor supporting home prices is the ongoing shortage of available homes. Several trends have contributed to this:

- Underbuilding after the 2008 housing crash

- High construction costs

- Homeowners locked into low mortgage rates

- Strong population growth in many regions

Because many homeowners refinanced into extremely low rates during the pandemic, they are reluctant to sell and take on a higher mortgage rate.

This has created what economists call a “lock-in effect.”

Fewer people are selling, which limits supply and keeps prices relatively stable.

Why Timing the Market Is So Difficult

Trying to perfectly time the housing market is extremely difficult-even for professionals. There are many variables involved, including:

- Interest rates

- Housing supply

- Local job growth

- Inflation

- Economic policy

- Consumer confidence

- Geopolitical factors

Waiting for the perfect moment can lead buyers to spend years on the sidelines while prices continue to move upward.

In many cases, buyers who purchased earlier-even with slightly higher interest rates-end up in a better long-term financial position.

Real Estate Is a Long-Term Investment

One of the most important principles in real estate is that time in the market usually matters more than timing the market.

Historically, home values have trended upward over long periods of time. While there are occasional market corrections, real estate has consistently been one of the most reliable ways to build long-term wealth.

Buying a home earlier allows homeowners to benefit from:

- Appreciation

- Equity growth

- Stable housing costs

- Tax advantages in some cases

Waiting indefinitely for the perfect interest rate may delay those benefits.

The Bottom Line for Buyers

Mortgage rates are an important factor when buying a home, but they should not be the only factor. Focusing exclusively on interest rates can cause buyers to overlook the bigger picture.

Here are the key takeaways:

- 3% mortgage rates were historically unusual.

- Waiting for those rates to return may take years.

- When rates fall, buyer demand typically increases.

- Increased demand often pushes home prices higher.

Buyers can refinance later if rates improve.

For many buyers, the smarter approach is to focus on finding the right home at the right price, rather than waiting indefinitely for the perfect interest rate.

Thinking About Buying?

If you’re considering buying a home and wondering how today’s mortgage rates affect your options, it’s worth having a conversation. Every buyer’s financial situation and timeline are different. Running the numbers based on your specific goals can help you determine the best strategy.

Whether you’re ready to buy now or simply exploring your options, having a clear plan can make all the difference.

If you’d like help analyzing today’s market or building a buying strategy, feel free to reach out anytime.

Please note: The opinions represented in this article are those of Jay Cottrell. They do not represent the opinions of LPT Realty, LLC or any of its other agents or affiliates.

—

Jay Cottrell | REALTOR® PSA®Broker Associate

LPT Realty, LLC

423-302-0862

Firm: 877-366-2213

www.tricities.homes